What Are Capital Controls?

The IMF recently published a report regarding the experiences that countries across the world have had with capital controls. The full document, entitled Country Experiences with the Use and Liberalization of Capital Controls, can be found on the IMF web page at http://www.imf.org/external/pubs/ft/op/op190/index.htm.

This FAQ summarizes key aspects of the IMF report. Please refer to the full document for further information.

I. What Are Capital Controls?

Capital controls restrict the free movement of capital. Countries use these controls to restrict volatile movements of capital entering (inflows) and exiting (outflows) their country. These increased volatile movements in capital can be attributed to the expanding global economy and a country's willingness to liberalize its financial system by allowing free convertibility of its currency. Analysts say currency convertibility has normally been allowed to finance current trade and direct investment transactions. Only recently has currency convertibility also been allowed in the capital account. By introducing this "capital account convertibility," countries expose themselves to autonomous inflows and outflows of funds (capital) by foreigners and locals, thus subjecting their currency to speculation and exchange rate volatility.

Restrictions can be placed on capital inflows and outflows. The IMF report states that most countries impose controls on inflows to respond to the macroeconomic implications of the increasing size and volatility of capital inflows. Outflow controls are used to limit the downward pressure on their currencies. Such controls are mainly applied to short-term capital transactions to counter speculative flows that threaten to undermine the stability of the exchange rate and deplete foreign exchange reserves.

A. Why Capital Controls?

The report states that many countries implement capital controls to help reconcile conflicting policy objectives when their exchange rate is fixed or heavily managed. The most common argument for the implementation of capital controls is to preserve the autonomy of monetary policy or of domestic objectives regarding direct monetary policy, as well as to reduce pressures on the exchange rate. A related argument is to protect monetary and financial stability during persistent capital flows. This is particularly important when there are concerns about the inflationary consequences of large capital inflows or when banks or the corporate sector inadequately assess their risk.

Inadequate assessment of risk typically occurs in the context of a heavily managed exchange rate that, by providing an implicit exchange rate guarantee, encourages a build-up of unhedged foreign currency positions. The report also states that capital controls have been used to support policies of financial repression to provide cheap financing for government budgets and priority sectors.

B. Types of Capital Controls

Capital controls encompass a wide range of diversified and often country-specific measures. These restrictions to capital movements usually take two broad forms: (a) "administrative" or direct controls and (b) "market-based" or indirect controls. Although these controls are usually applied separately during heavy capital flows, they are often applied in tandem.

Administrative or direct controls restrict capital transactions and associated payments and transfer of funds through outright prohibitions. These controls are designed to directly affect the volume of cross-border financial transactions.

They typically impose administrative obligations on a country's banking system to control the flows of capital.

Market-based or indirect controls make transactions more costly thereby discouraging capital movement and the associated transactions. These capital controls may take the form of dual or multiple exchange rate systems, explicit taxation of cross-border financial flows, indirect taxation of cross-border flows and other indirect regulatory controls.

II. Disadvantages

The report states that regardless of whether capital controls are effective, their use may come at a cost. First, restrictions on capital flows, particularly when they are comprehensive or wide-ranging, may interfere with desirable capital and current transactions along with less desirable ones.

Second, controls may entail non-trivial administration costs for effective implementation, particularly when the measures have to be broadened to close potential loopholes for circumvention.

Third, there is also the risk that shielding the domestic financial markets by capital controls may postpone necessary adjustments in policies or hamper private-sector adaptation to changing international circumstances.

Finally, controls may give rise to negative market perceptions, which may in turn make it costlier and more difficult for the country to access foreign funds.

III. Conclusions of Report

The effectiveness of the controls to achieve their intended objectives has been mixed. In most countries, the controls had some effect initially, but fell short of meeting each country's objectives. The report further breaks down its conclusions into short-term capital inflows and capital outflows.

A. Capital Inflows

The report suggests two tentative conclusions. First, to be effective, the coverage of controls needs to be comprehensive and the controls need to be implemented forcefully. Considerable administrative costs are incurred in continuously extending, amending, and monitoring compliance with the regulations. Second, although capital controls appeared to be effective in some countries, it is difficult to be certain of their role given the problems involved in disentangling the impact of the controls from that of the accompanying policies, which included the strengthening of prudential regulations, greater exchange rate flexibility and adjustment in monetary policy, as they are often imposed and modified for macroeconomic rather than microeconomic reasons, for example, at times of downward pressure on exchange rates.

B. Capital Outflows

The reimposition of controls on capital outflows during episodes of financial crisis has provided only a temporary respite of varying duration to the authorities. The experiences of the countries studied suggests that: (a) to be effective, the controls must be comprehensive, strongly enforced and accompanied by necessary reforms and policy adjustments; (b) controls do not provide lasting protections in the face of sufficient incentives for circumvention (in particular, attractive return differentials in the offshore markets and strong market expectations of currency depreciation); (c) the ability to control offshore market activity may have been instrumental in containing outflows and stemming speculative pressures; and (d) effective measures risk discouraging legitimate transactions, including foreign direct investment and trade-related hedging transactions and may raise the cost of accessing international capital markets.

Source...click here

International Rules for Capital Controls

Although economists generally agree that countries can derive substantial gains from international economic integration, the extent to which they should open themselves to international capital flows remains a controversial issue.

There is still, 20 years after the rise of emerging markets finance, a wide diversity of approaches to capital account policies. Some emerging market economies maintain a completely open capital account. Others, most notably Brazil, have experimented more actively with market-based prudential capital controls since the crisis. And still other countries, such as China, maintain tight restrictions on their capital account.

There has also been a shift in official views on this topic, which have become more sympathetic to capital controls (Ostry et al. 2011; IMF 2011). Unlike for trade in goods, however, there are no international rules to constrain, discipline, or indeed legitimise restrictions that countries put on their capital account.1 In our monograph Who Needs to Open the Capital Account? (Jeanne et al. 2012), we present the case for developing international rules for capital flows.

The case for prudential capital controls

The pros and cons of prudential capital controls to curb the boom-bust cycle in capital flows have been discussed before (Williamson 2005), but economists now understand better the theoretical case for such policies with a new literature on the welfare economics of prudential capital controls (Korinek 2011). This literature essentially transposes to international capital flows the closed-economy analysis of the macroprudential policies that aim to curb the boom-bust cycle in credit and asset prices. It finds that it is optimal to impose a countercyclical Pigouvian tax on debt inflows in a boom to reduce the risk and severity of a bust. Interestingly, the optimal tax would fall primarily on the flows (short-term or foreign currency debt) that are the least likely to be conducive to economic growth. The optimal tax has also been quantified in calibrated dynamic welfare optimising models. Models with endogenous and occasionally binding constraints are not tractable and must be simplified in some respects to be solvable, even numerically, but the results may be informative.

A nice example of this approach is Bianchi (2011), who finds, in a model calibrated to Argentina, that the optimal tax rate on one-year foreign currency debt increases with the country's indebtedness and fluctuates between 0% and a maximum of 22%. Obviously, capital controls are not a silver bullet.

Like any attempt to regulate the financial sector, they elicit attempts to circumvent or evade and can be used effectively only if they are used with moderation. But this observation applies to all taxes and regulations. Capital controls are not a panacea, but this does not prevent them from being a legitimate instrument in the macroprudential toolbox. Capital account policies and trade distortions The international community invests considerably more effort in maintaining a level playing field for international trade in goods than for international trade in assets. One could argue that this is justified by the fact that the gains from free trade seem much larger for the former than for the latter (Bhagwati 1998). And Chapter 3 of our book, which uses a “meta-regression” approach incorporating a large number of empirical specifications, confirms the finding in most of the literature: free capital mobility has little impact on economic development (although there is some evidence that foreign direct investment and stock market liberalisation may, at least temporarily, raise growth). The problem about using this finding to be agnostic or permissive about capital account restrictions is that those restrictions can be used to distort real exchange rates to the advantage of the countries that impose them. This contradicts the purpose of trade rules and over time may erode the support for free trade. China, because of its importance in the global economy, is the most significant example. It would be an exaggeration to describe the Chinese capital account as closed, if only because China receives large amounts of foreign direct investment (and even encourages it through tax incentives). But China severely restricts other forms of capital inflows, and controls its outflows too.

Most of the Chinese foreign assets are accumulated as international reserves, which the authorities have accumulated in large quantities. However, full control over capital flows implies full control over its macroeconomic doppelganger, the trade balance, and hence the real exchange rate.

Under some conditions, as shown in Jeanne (2011), full control over the capital account allows the authorities to undervalue the real exchange rate and affect trade flows in the same way as they would with import tariffs and export subsidies. The case for international rules Currently, the international regime is permissive about the use of capital controls: countries can use them or not as they wish. We view this status quo as problematic and see compelling reasons to establish an international regime for capital flows.

First, the lack of commonly agreed rules implies that capital controls are still marked by a certain stigma, so that the appropriate policies may be pursued with less than optimal vigour. But we also argue that an international regime for capital flows should go further, and take appropriate account of spill-over effects. This is particularly the case of policies that repress domestic demand and, through a combination of reserve accumulation and restrictions on inflows, maintain a current account surplus.

Those policies have the same economic effects as trade protectionism and undermine the global public good of free trade. But the point may apply also to prudential capital controls. As recently shown by Forbes et al (2012) in the case of Brazil, capital account restrictions are liable to divert capital flows from one recipient to another, and thereby give third countries a strong interest in the controls imposed by others.

The implications of this argument have not yet been absorbed by the profession, but it seems possible that they will turn out to be significant for the optimal international design of capital account policies. As for trade in goods, if there are controls, we would be strongly in favour of having transparent, price-based measures, such as a countercyclical tax on certain types of capital flows. The international community could agree on a ceiling on the tax rate to ensure that the harmful effects of controls (if any) would be limited. The new rules could be embodied in an international code of good practices developed under the auspices of the IMF. In a world where capital and trade flows have become so linked, the asymmetry of the status quo comprising permissiveness toward the former and strict regulation of the latter is increasingly untenable.

Source...click here

There is still, 20 years after the rise of emerging markets finance, a wide diversity of approaches to capital account policies. Some emerging market economies maintain a completely open capital account. Others, most notably Brazil, have experimented more actively with market-based prudential capital controls since the crisis. And still other countries, such as China, maintain tight restrictions on their capital account.

There has also been a shift in official views on this topic, which have become more sympathetic to capital controls (Ostry et al. 2011; IMF 2011). Unlike for trade in goods, however, there are no international rules to constrain, discipline, or indeed legitimise restrictions that countries put on their capital account.1 In our monograph Who Needs to Open the Capital Account? (Jeanne et al. 2012), we present the case for developing international rules for capital flows.

The case for prudential capital controls

The pros and cons of prudential capital controls to curb the boom-bust cycle in capital flows have been discussed before (Williamson 2005), but economists now understand better the theoretical case for such policies with a new literature on the welfare economics of prudential capital controls (Korinek 2011). This literature essentially transposes to international capital flows the closed-economy analysis of the macroprudential policies that aim to curb the boom-bust cycle in credit and asset prices. It finds that it is optimal to impose a countercyclical Pigouvian tax on debt inflows in a boom to reduce the risk and severity of a bust. Interestingly, the optimal tax would fall primarily on the flows (short-term or foreign currency debt) that are the least likely to be conducive to economic growth. The optimal tax has also been quantified in calibrated dynamic welfare optimising models. Models with endogenous and occasionally binding constraints are not tractable and must be simplified in some respects to be solvable, even numerically, but the results may be informative.

A nice example of this approach is Bianchi (2011), who finds, in a model calibrated to Argentina, that the optimal tax rate on one-year foreign currency debt increases with the country's indebtedness and fluctuates between 0% and a maximum of 22%. Obviously, capital controls are not a silver bullet.

Like any attempt to regulate the financial sector, they elicit attempts to circumvent or evade and can be used effectively only if they are used with moderation. But this observation applies to all taxes and regulations. Capital controls are not a panacea, but this does not prevent them from being a legitimate instrument in the macroprudential toolbox. Capital account policies and trade distortions The international community invests considerably more effort in maintaining a level playing field for international trade in goods than for international trade in assets. One could argue that this is justified by the fact that the gains from free trade seem much larger for the former than for the latter (Bhagwati 1998). And Chapter 3 of our book, which uses a “meta-regression” approach incorporating a large number of empirical specifications, confirms the finding in most of the literature: free capital mobility has little impact on economic development (although there is some evidence that foreign direct investment and stock market liberalisation may, at least temporarily, raise growth). The problem about using this finding to be agnostic or permissive about capital account restrictions is that those restrictions can be used to distort real exchange rates to the advantage of the countries that impose them. This contradicts the purpose of trade rules and over time may erode the support for free trade. China, because of its importance in the global economy, is the most significant example. It would be an exaggeration to describe the Chinese capital account as closed, if only because China receives large amounts of foreign direct investment (and even encourages it through tax incentives). But China severely restricts other forms of capital inflows, and controls its outflows too.

Most of the Chinese foreign assets are accumulated as international reserves, which the authorities have accumulated in large quantities. However, full control over capital flows implies full control over its macroeconomic doppelganger, the trade balance, and hence the real exchange rate.

Under some conditions, as shown in Jeanne (2011), full control over the capital account allows the authorities to undervalue the real exchange rate and affect trade flows in the same way as they would with import tariffs and export subsidies. The case for international rules Currently, the international regime is permissive about the use of capital controls: countries can use them or not as they wish. We view this status quo as problematic and see compelling reasons to establish an international regime for capital flows.

First, the lack of commonly agreed rules implies that capital controls are still marked by a certain stigma, so that the appropriate policies may be pursued with less than optimal vigour. But we also argue that an international regime for capital flows should go further, and take appropriate account of spill-over effects. This is particularly the case of policies that repress domestic demand and, through a combination of reserve accumulation and restrictions on inflows, maintain a current account surplus.

Those policies have the same economic effects as trade protectionism and undermine the global public good of free trade. But the point may apply also to prudential capital controls. As recently shown by Forbes et al (2012) in the case of Brazil, capital account restrictions are liable to divert capital flows from one recipient to another, and thereby give third countries a strong interest in the controls imposed by others.

The implications of this argument have not yet been absorbed by the profession, but it seems possible that they will turn out to be significant for the optimal international design of capital account policies. As for trade in goods, if there are controls, we would be strongly in favour of having transparent, price-based measures, such as a countercyclical tax on certain types of capital flows. The international community could agree on a ceiling on the tax rate to ensure that the harmful effects of controls (if any) would be limited. The new rules could be embodied in an international code of good practices developed under the auspices of the IMF. In a world where capital and trade flows have become so linked, the asymmetry of the status quo comprising permissiveness toward the former and strict regulation of the latter is increasingly untenable.

Source...click here

For and against Capital controls

Full freedom of movement for capital and payments has so far only been approached between individual pairings of states which have free trade agreements and relative freedom from capital controls, such as Canada and the U.S., or the complete freedom within regions such as the European Union, with its "Four Freedoms" and the Eurozone. During the first age of globalization that was brought to an end by World War I, there were very few restrictions on the movement of capital, but all major economies except for Great Britain and the Netherlands heavily restricted payments for goods by the use of current account controls such as tariffs and duties.[8]

[edit]Arguments in favour of free capital movement

Pro free market economists claim the following advantages for free movement of capital:

- It enhances the general economic welfare by allowing savings to be channelled to their most productive use.[28]

- By encouraging foreign direct investment it helps developing economies to benefit from foreign expertise.[28]

- Allows states to raise funds from external markets to help them mitigate a temporary recession.[28]

- Enables both savers and borrowers to secure the best available market rate.[12]

- When controls include taxes, funds raised are sometimes siphoned off by corrupt government officials for their personal use.[12]

- Hawala-type traders across Asia have always been able to evade currency movement controls

- Computer and satellite communication technologies have made Electronic funds transfer a convenience for increasing numbers of bank customers.

[edit]Arguments in favour of capital controls

Pro capital control economists have made the following points.

- Capital controls may represent an optimal Macroprudential policy that reduces the risk of financial crises and prevents the associated externalities.[3] [50] [62] [63]

- Global economic growth was on average considerably higher in the Bretton Woods periods where capital controls were widely in use. Using Regression analysis, economists such as Dani Rodrik have found no positive correlation between growth and free capital movement.[28]

- Capital controls limiting a nation's residents from owning foreign assets can ensure that domestic credit is available more cheaply than would otherwise be the case. This sort of capital control is still in effect in both India and China. In India the controls encourage residents to provide cheap funds directly to the government, while in China it means that Chinese businesses have an inexpensive source of loans.[23]

- Economic crises have been considerably more frequent since the Bretton Woods capital controls were relaxed. Even economic historians who class capital controls as repressive have concluded capital controls, more than the period's high growth, were responsible for the infrequency of crisis.[23] Studies have found that large uncontrolled capital inflows have frequently damaged a nation's economic development by causing its currency to appreciate, by contributing to inflation, and by causing unsustainable economic booms which often precede financial crises - caused when the inflows sharply reverse and both domestic and foreign capital flee the country. The risk of crisis is especially high in developing economies where the inbound flows become loans denominated in foreign currency, so that the repayments become considerably more expensive as the developing country's currency depreciates. This is known as original Sin (economics).[8][64][65]

What are capital controls?

Capital controls are residency-based measures such as transaction taxes and other limits or outright prohibitions, which a nation's government can use to regulate flows from capital markets into and out of the country's capital account.

These measures may be economy-wide, sector-specific (usually the financial sector), or industry specific (for example, “strategic” industries). They may apply to all flows, or may differentiate by type or duration of the flow (debt, equity, direct investment; short-term vs. medium- and long-term).

Types of capital control include exchange controls that prevent or limit the buying and selling of a national currency at the market rate, caps on the allowed volume for the international sale or purchase of various financial assets, transaction taxes such as the proposed Tobin tax, minimum stay requirements, requirements for mandatory approval, or even limits on the amount of money a private citizen is allowed to remove from the country.

There have been several shifts of opinion on whether capital controls are beneficial and in what circumstances they should be used. Capital controls were an integral part of the Bretton Woods system which emerged after World War II and lasted until the early 1970s. This period was the first time capital controls had been endorsed by mainstream economics. In the 1970s free market economists became increasingly successful in persuading their colleagues that capital controls were in the main harmful. The US, other western governments, and the international financial institutions (the International Monetary Fund (IMF) and World Bank) began to take an increasingly critical view of capital controls and persuaded many countries to abandon them to reap the benefits of financial globalization.[1] The Latin American debt crisis of the early 1980s, the East Asian Financial Crisis of the late 1990s, the Russian Ruble crisis of 1998-99, and the Global Financial Crisis of 2008, however, highlighted the risks associated with the volatility of capital flows, and led many countries—even those with relatively open capital accounts—to make use of capital controls alongside macroeconomic and prudential policies as means to dampen the effects of volatile flows on their economies. In the aftermath of the Global Financial Crisis, as capital inflows surged to emerging market economies, a group of economists at the IMF outlined the elements of a policy toolkit to manage the macroeconomic and financial-stability risks associated with capital flow volatility, and the role of capital controls within that toolkit.[2] The study, as well as a successor study focusing on financial-stability concerns stemming from capital flow volatility,[3] while not representing an IMF official view, were nevertheless influential in generating debate among policy makers and the international community, and ultimately in bringing about a shift in the institutional position of the IMF.[4][5][6] With the increased use of capital controls in recent years, the IMF has moved to destigmatize the use of capital controls alongside macroeconomic and prudential policies to deal with capital flow volatility. More widespread use of the capital controls instrument, however, raises a host of multilateral coordination issues, as enunciated for example by the G-20, echoing the concerns voiced by Keynes and White more than six decades ago.[7

The links refer to this article

These measures may be economy-wide, sector-specific (usually the financial sector), or industry specific (for example, “strategic” industries). They may apply to all flows, or may differentiate by type or duration of the flow (debt, equity, direct investment; short-term vs. medium- and long-term).

Types of capital control include exchange controls that prevent or limit the buying and selling of a national currency at the market rate, caps on the allowed volume for the international sale or purchase of various financial assets, transaction taxes such as the proposed Tobin tax, minimum stay requirements, requirements for mandatory approval, or even limits on the amount of money a private citizen is allowed to remove from the country.

There have been several shifts of opinion on whether capital controls are beneficial and in what circumstances they should be used. Capital controls were an integral part of the Bretton Woods system which emerged after World War II and lasted until the early 1970s. This period was the first time capital controls had been endorsed by mainstream economics. In the 1970s free market economists became increasingly successful in persuading their colleagues that capital controls were in the main harmful. The US, other western governments, and the international financial institutions (the International Monetary Fund (IMF) and World Bank) began to take an increasingly critical view of capital controls and persuaded many countries to abandon them to reap the benefits of financial globalization.[1] The Latin American debt crisis of the early 1980s, the East Asian Financial Crisis of the late 1990s, the Russian Ruble crisis of 1998-99, and the Global Financial Crisis of 2008, however, highlighted the risks associated with the volatility of capital flows, and led many countries—even those with relatively open capital accounts—to make use of capital controls alongside macroeconomic and prudential policies as means to dampen the effects of volatile flows on their economies. In the aftermath of the Global Financial Crisis, as capital inflows surged to emerging market economies, a group of economists at the IMF outlined the elements of a policy toolkit to manage the macroeconomic and financial-stability risks associated with capital flow volatility, and the role of capital controls within that toolkit.[2] The study, as well as a successor study focusing on financial-stability concerns stemming from capital flow volatility,[3] while not representing an IMF official view, were nevertheless influential in generating debate among policy makers and the international community, and ultimately in bringing about a shift in the institutional position of the IMF.[4][5][6] With the increased use of capital controls in recent years, the IMF has moved to destigmatize the use of capital controls alongside macroeconomic and prudential policies to deal with capital flow volatility. More widespread use of the capital controls instrument, however, raises a host of multilateral coordination issues, as enunciated for example by the G-20, echoing the concerns voiced by Keynes and White more than six decades ago.[7

The links refer to this article

Banking crisis - explained

Young Paddy bought a donkey from a farmer for £100.

The farmer agreed to deliver the donkey the next day..... The next day he drove up and said, 'Sorry son, but I have some bad news. The donkey's dead.'

Paddy replied, 'Well then just give me my money back.'

The farmer said, 'Can't do that. I've already spent it.' Paddy said, 'OK, then, just bring me the dead donkey.'

The farmer asked, 'What are you going to do with him?'

Paddy said, 'I'm going to raffle him off.'

The farmer said, 'You can't raffle a dead donkey!'

Paddy said, 'Sure I can. Watch me. I just won't tell anybody he's dead.'

A month later, the farmer met up with Paddy and asked, 'What happened with that dead donkey?'

Paddy said, 'I raffled him off. I sold 500 tickets at two pounds a piece and made a profit of £898' The farmer said, 'Didn't anyone complain?'

Paddy said, 'Just the guy who won. So I gave him his two pounds back.'

Paddy now works for the Royal Bank of Scotland .

Now watch a video:

The farmer agreed to deliver the donkey the next day..... The next day he drove up and said, 'Sorry son, but I have some bad news. The donkey's dead.'

Paddy replied, 'Well then just give me my money back.'

The farmer said, 'Can't do that. I've already spent it.' Paddy said, 'OK, then, just bring me the dead donkey.'

The farmer asked, 'What are you going to do with him?'

Paddy said, 'I'm going to raffle him off.'

The farmer said, 'You can't raffle a dead donkey!'

Paddy said, 'Sure I can. Watch me. I just won't tell anybody he's dead.'

A month later, the farmer met up with Paddy and asked, 'What happened with that dead donkey?'

Paddy said, 'I raffled him off. I sold 500 tickets at two pounds a piece and made a profit of £898' The farmer said, 'Didn't anyone complain?'

Paddy said, 'Just the guy who won. So I gave him his two pounds back.'

Paddy now works for the Royal Bank of Scotland .

Now watch a video:

IS-LM Model

The IS LM Model explained

The best way to revise a concept is to write about it! Paul Krugman has this description of the IS (investment-savings)-LM (liquidity preference-money supply) model that examines the interaction between the market for goods and services and the money market,

My favorite approach is to think of IS-LM as a way to reconcile two seemingly incompatible views about what determines interest rates. One view says that the interest rate is determined by the supply of and demand for savings – the “loanable funds” approach. The other says that the interest rate is determined by the tradeoff between bonds, which pay interest, and money, which doesn’t, but which you can use for transactions and therefore has special value due to its liquidity – the “liquidity preference” approach...

loanable funds or liquidity preference doesn’t determine the interest rate per se; they determine a set of possible combinations of the interest rate and GDP, with lower rates corresponding to higher GDP... the adjustment of GDP is what makes both loanable funds and liquidity preference hold at the same time.

Let us analayze both models. Consider the loanable funds first. As interest rates fall (for whatever reason), investment increases, economy expands, and income levels increase. Atleast some portion of increased income will be saved, thereby expanding the savings pool available. A new interest rate equilibrium develops at this lower rate level between investment demand and savings available. The IS curve "determines a set of possible combinations of the interest rate and GDP, with lower rates corresponding to higher GDP" (therefore downward slope for the IS curve).

Now for the liquidity preference model. People make trade-offs (assuming the same risk, between returns and liquidity) when they take decisions to allocate their wealth between different investment and savings options (specifically between money and bonds). For a particular instrument, if its returns rise, people become willing to settle for lower liquidity. If the central bank wants to increase the money supply (cash balances with people), it must lower interest rates so as to induce people to increase their preference for liquidity. The liquidity preference curve is thererefore downward sloping.

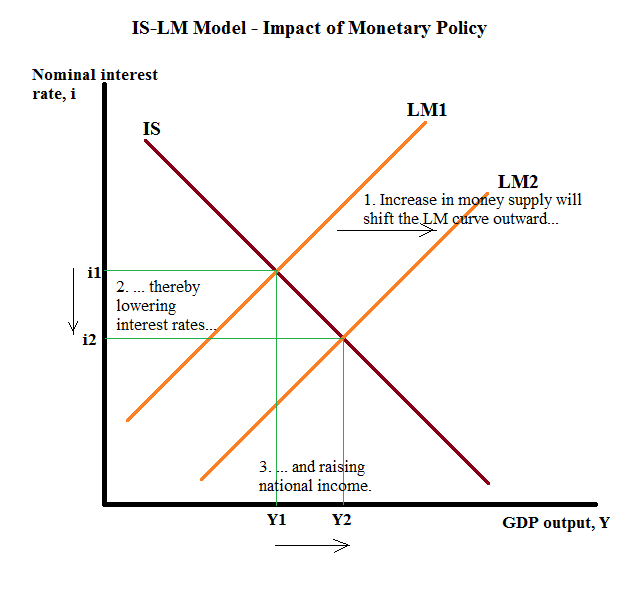

In the market for money supply (from central banks and passed on through commercial banks) and money demand (or liquidity preference), the former is vertical (in the short run, central banks can hold the money supply constant, even without changing the interest rate) while the latter is downward sloping. An increase in GDP, as indicated in the graphic above, will result in greater number of spending transactions, higher demand for money, and therefore a shift in the liquidity preference function outward. If the real money supply (supply adjusted for inflation) is held constant and the market has to equilibriate, the higher demand for money will have to be accompanied by an increase in interest rates. The LM curve, which is the set of all possible combinations of the interest rate and GDP where the money supply and demand matches, therefore slopes upward.

At the equilibrium of IS-LM graph, the loanable funds (goods/services market) and liquidity preference (money market) are in balance. Now let us examine the effects of fiscal and monetary policy on the economy by using the IS-LM model. Fiscal Policy first. Anything which causes a change in consumption, government spending, or investments, will shift the IS curve. A rise in Government investment spending, by increasing the demand for goods at the same interest rate, has the effect of pushing the IS curve to the right. This in turn increases the aggregate demand and therefore the GDP. However, interest rates have to increase so as to equilibriate between the loanable funds and liquidity preferences.

The classical economists refute this and argue that the resulting higher interest rates will eventually crowd-out private consumption and investment, thereby putting downward pressure on the growth of economic output. Further, the higher government spending will trigger inflationary pressures, which in turn will shift the LM curve inwards, thereby raising interest rates. These twin dangers, they contend, will invariably strangulate growth.

Similarly with monetary policy, as the money supply is increased, the LM curve shifts outward or downward. This in turn will lower interest rates, spur investments and consumption, and raise national income.

In both cases, exogenous shocks/events can lead to changes in liquidity preference and demand for savings, which in turn can shift the LM or IS curves respectively. However, in the long-run, prices/wages adjust to return the real money supply curve (and thereby the LM curve) backwards to its original position. It is therefore argued that the long-run impact of any change in monetary policy is minimal. But the fine print of the debate is about the magnitude of the adjustment in prices/wages and the time taken for this adjustment (or what constitutes long-term). Classicists claim that prices adjust quickly whereas Keynesians argue that prices are sticky.

Similarly, when the economy faces conditions like the present situation - frozen credit markets, reduced investment and consumption apetite, very high unemployment rate, and zero interest rate bound - many of the standard assumptions of classical economics breaks down. In the circumstances, government is the only agent with the ability to pull the economy. Further, since the economy is operating way below its potential output frontier, large pool of labour unemployed, and aggregate demand heavily constrained by lack of purchasing power, an increase in money supply is not going to lead to inflationary pressures. Also, at the zero-bound, since cash and bonds become interchangeable, at the margins, money is just being held as a store of value, and changes in the money supply have no effect.

The above is from here - an excellent blog to follow

Of course if you would like to get complicated and look at modern macroeconomic phenomena...

Here are some notes you may wish to print out on the IS-LM curve...

Lastly...a video

Liquidity Preference Theory

According to Keynes interest is purely a monetary phenomenon because rate of interest is calculated in terms of money.

It is a monetary phenomenon in the sense that rate of interest is determined by the supply of and demand for money, Keynes defined interest as the reward for parting with liquidity for specified time.

What is liquidity preference:-

Liquidity means shift ability without loss. It refers to easy convertibility. Money is the most liquid assets. Money commands universal acceptability. Everybody likes to hold assets in form of cash money. If at all they surrender this liquidity they must be paid interest. As water is liquid and it can be used for anything at will, so also money can be converted to anything immediately.

Other costly assets like gold and landed property may be valuable but they cannot be shifted at will.

Thus they lack liquidity.

As money are highly liquid people to hold money with than in form of Cash. This preference according to Keynes is popularly called liquidity preference.

Thus according to Keynes interest is the price paid for surrendering their liquid assets. Greater the liquidity preference higher shall be the rate of interest. The liquidity preference constitutes the demand for money. According Keynes rate of interest is demand by the supply of and demand for money. The rate of interest on the demand side is governed by the liquidity preference of the community arises due to the necessity of keeping cash for meeting certain requirements.

The demand for liquidity arises due to three motives.

Demand for money:

(a) The transaction motive:- An individual for his day to day transaction demand money. A man has to buy food and medicines in his day to day life. For this purpose people want to keep some cash with them. The amount of cash which an individual will require to keep in his possession depends on two factors (i) the size of personal income and (ii) the length of the time between pay-days. The richer a community the greater the demand for transaction motive.

(b) The precautionary motive: People demand to hold money with them to meet the unforeseen contingencies. An individual may become unemployed; he may fall sick or may meet serious accident. For all these misfortune, he demands money to hold with him. The amount of money under the precautionary motive depends on the individual's condition, economic as well as political which he lives. Thus the demand for money under this motive depends on size of income, nature of the person and farsightedness.

(c) Speculative motive: Under speculative motive people want to keep each with them to take advantage of the charges in the price of bonds and securities. People under speculative motive hold money in order to secure profit from the future speculation of the bond market. If the prices of bonds and securities are expected to rise speculative will like to buy them. In such a situation the demand to hold cash diminishes. Thus liquidity preference will be more at lower interest rates.

Money under the above three motives constitute the demand for money.

An increase in the demand for money leads to a rise in the late of interest, a decrease in the demand for money leads to a fall in the rate of interest. According to Keynes the first two motives for liquidity preference namely the transaction and precautionary are interest inelastic. That is why the speculative motive is important in the sense that speculative motive is interest elastic.

Supply money: The supply of money is different from the supply of ordinary commodity. The supply of commodity is a flow whereas the supply of money is a stock. The aggregate supply of money in a community at any time is the sum of money stock of all the members of the society. The supply of money is controlled by the govt. The supply of money in existence consists of legal tender money, bank money and credit money. The supply of money is determined by the central bank of a country. The total supply of money is fixed at a particular point of time. The supply of money is not influenced by the rate of interest.

Equilibrium rate of interest: The rate of interest is determined by the demand for money and supply of money. The equilibrium rate of interest is fixed at that point where supply of and demands for money are equal. If the rate of interest is high peoples demand for money (liquidity preference) is low. The liquidity preference function or demand curve states that when interest rate falls, the demand to hold money increases and when interest rate raises the demand for money, diminishes. The determination of the rate of interest can be better explained in the shop.

Now here's a practical part - draw your own diagram for the details below!

In the above figure OX-axis measures the supply of money and OY-axis represents the rate of interest. The LP curve represents liquidity preference curve. This curve represents the demand for money at various rate of interest. The total supply of money is represented by a vertical line Ms. The equilibrium rate of interest is determined at that level. Where the demand for money is equal to supply of money. Given the demand for money when supply of money rises, rate of interest falls to OR. With a fall in money supply rate of interest rises. Similarly the liquidity preference may change given the supply of money. When liquidity preference shifts upward, given the supply money at the level on the rate of interest rises to the level OQ. Thus according to Keynes interact is purely a monetary phenomenon.

Source is here

Now watch a video....

Now read some more notes...

KEYNES’ LIQUIDITY PREFERENCE THEORY OF INTEREST

Keynes defines the rate of interest as the reward for parting with liquidity for a specified period of time. According to him, the rate of interest is determined by the demand for and supply of money.

Demand for money: Liquidity preference means the desire of the public to hold cash. According to Keynes, there are three motives behind the desire of the public to hold liquid cash: (1) the transaction motive, (2) the precautionary motive, and (3) the speculative motive. Transactions Motive: The transactions motive relates to the demand for money or the need of cash for the current transactions of individual and business exchanges. Individuals hold cash in order to bridge the gap between the receipt of income and its expenditure. This is called the income motive. The businessmen also need to hold ready cash in order to meet their current needs like payments for raw materials, transport, wages etc. This is called the business motive.

Precautionary motive: Precautionary motive for holding money refers to the desire to hold cash balances for unforeseen contingencies. Individuals hold some cash to provide for illness, accidents, unemployment and other unforeseen contingencies. Similarly, businessmen keep cash in reserve to tide over unfavourable conditions or to gain from unexpected deals. Keynes holds that the transaction and precautionary motives are relatively interest inelastic, but are highly income elastic.

The amount of money held under these two motives (M1) is a function (L1) of the level of income (Y) and is expressed as M1 = L1 (Y) Speculative Motive: The speculative motive relates to the desire to hold one’s resources in liquid form to take advantage of future changes in the rate of interest or bond prices. Bond prices and the rate of interest are inversely related to each other. If bond prices are expected to rise, i.e., the rate of interest is expected to fall, people will buy bonds to sell when the price later actually rises. If, however, bond prices are expected to fall, i.e., the rate of interest is expected to rise, people will sell bonds to avoid losses.

According to Keynes, the higher the rate of interest, the lower the speculative demand for money, and lower the rate of interest, the higher the speculative demand for money. Algebraically, Keynes expressed the speculative demand for money as M2 = L2 (r) Where, L2 is the speculative demand for money, and r is the rate of interest. Geometrically, it is a smooth curve which slopes downward from left to right. Now, if the total liquid money is denoted by M, the transactions plus precautionary motives by M1 and the speculative motive by M2, then M = M1 + M2. Since M1 = L1 (Y) and M2 = L2 (r), the total liquidity preference function is expressed as M = L (Y, r).

Supply of Money: The supply of money refers to the total quantity of money in the country. Though the supply of money is a function of the rate of interest to a certain degree, yet it is considered to be fixed by the monetary authorities. Hence the supply curve of money is taken as perfectly inelastic represented by a vertical straight line. Determination of the Rate of Interest: Like the price of any product, the rate of interest is determined at the level where the demand for money equals the supply of money. In the following figure, the vertical line QM represents the supply of money and L the total demand for money curve. Both the curve intersect at E2 where the equilibrium rate of interest OR is established.

If there is any deviation from this equilibrium position an adjustment will take place through the rate of interest, and equilibrium E2 will be re-established.

At the point E1 the supply of money OM is greater than the demand for money OM1. Consequently, the rate of interest will start declining from OR1 till the equilibrium rate of interest OR is reached.

If there is any deviation from this equilibrium position an adjustment will take place through the rate of interest, and equilibrium E2 will be re-established.

At the point E1 the supply of money OM is greater than the demand for money OM1. Consequently, the rate of interest will start declining from OR1 till the equilibrium rate of interest OR is reached.

Similarly at OR2 level of interest rate, the demand for money OM2 is greater than the supply of money OM. As a result, the rate of interest OR2 will start rising till it reaches the equilibrium rate OR. It may be noted that, if the supply of money is increased by the monetary authorities, but the liquidity preference curve L remains the same, the rate of interest will fall. If the demand for money increases and the liquidity preference curve sifts upward, given the supply of money, the rate of interest will rise.

Criticisms: Keynes theory of interest has been criticized on the following grounds:

1. It has been pointed out that the rate of interest is not purely a monetary phenomenon. Real forces like productivity of capital and thriftiness or saving by the people also play an important role in the determination of the rate of interest.

2. Liquidity preference is not the only factor governing the rate of interest. There are several other factors which influence the rate of interest by affecting the demand for and supply of investible funds.

3. The liquidity preference theory does not explain the existence of different rates of interest prevailing in the market at the same time.

4. Keynes ignores saving or waiting as a means or source of investible fund. To part with liquidity without there being any saving is meaningless.

5. The Keynesian theory only explains interest in the short-run. It gives no clue to the rates of interest in the long run.

6. Keynes theory of interest, like the classical and loanable funds theories, is indeterminate. We cannot know how much money will be available for the speculative demand for money unless we know how much the transaction demand for money is.

Read more...

It is a monetary phenomenon in the sense that rate of interest is determined by the supply of and demand for money, Keynes defined interest as the reward for parting with liquidity for specified time.

What is liquidity preference:-

Liquidity means shift ability without loss. It refers to easy convertibility. Money is the most liquid assets. Money commands universal acceptability. Everybody likes to hold assets in form of cash money. If at all they surrender this liquidity they must be paid interest. As water is liquid and it can be used for anything at will, so also money can be converted to anything immediately.

Other costly assets like gold and landed property may be valuable but they cannot be shifted at will.

Thus they lack liquidity.

As money are highly liquid people to hold money with than in form of Cash. This preference according to Keynes is popularly called liquidity preference.

Thus according to Keynes interest is the price paid for surrendering their liquid assets. Greater the liquidity preference higher shall be the rate of interest. The liquidity preference constitutes the demand for money. According Keynes rate of interest is demand by the supply of and demand for money. The rate of interest on the demand side is governed by the liquidity preference of the community arises due to the necessity of keeping cash for meeting certain requirements.

The demand for liquidity arises due to three motives.

Demand for money:

(a) The transaction motive:- An individual for his day to day transaction demand money. A man has to buy food and medicines in his day to day life. For this purpose people want to keep some cash with them. The amount of cash which an individual will require to keep in his possession depends on two factors (i) the size of personal income and (ii) the length of the time between pay-days. The richer a community the greater the demand for transaction motive.

(b) The precautionary motive: People demand to hold money with them to meet the unforeseen contingencies. An individual may become unemployed; he may fall sick or may meet serious accident. For all these misfortune, he demands money to hold with him. The amount of money under the precautionary motive depends on the individual's condition, economic as well as political which he lives. Thus the demand for money under this motive depends on size of income, nature of the person and farsightedness.

(c) Speculative motive: Under speculative motive people want to keep each with them to take advantage of the charges in the price of bonds and securities. People under speculative motive hold money in order to secure profit from the future speculation of the bond market. If the prices of bonds and securities are expected to rise speculative will like to buy them. In such a situation the demand to hold cash diminishes. Thus liquidity preference will be more at lower interest rates.

Money under the above three motives constitute the demand for money.

An increase in the demand for money leads to a rise in the late of interest, a decrease in the demand for money leads to a fall in the rate of interest. According to Keynes the first two motives for liquidity preference namely the transaction and precautionary are interest inelastic. That is why the speculative motive is important in the sense that speculative motive is interest elastic.

Supply money: The supply of money is different from the supply of ordinary commodity. The supply of commodity is a flow whereas the supply of money is a stock. The aggregate supply of money in a community at any time is the sum of money stock of all the members of the society. The supply of money is controlled by the govt. The supply of money in existence consists of legal tender money, bank money and credit money. The supply of money is determined by the central bank of a country. The total supply of money is fixed at a particular point of time. The supply of money is not influenced by the rate of interest.

Equilibrium rate of interest: The rate of interest is determined by the demand for money and supply of money. The equilibrium rate of interest is fixed at that point where supply of and demands for money are equal. If the rate of interest is high peoples demand for money (liquidity preference) is low. The liquidity preference function or demand curve states that when interest rate falls, the demand to hold money increases and when interest rate raises the demand for money, diminishes. The determination of the rate of interest can be better explained in the shop.

Now here's a practical part - draw your own diagram for the details below!

In the above figure OX-axis measures the supply of money and OY-axis represents the rate of interest. The LP curve represents liquidity preference curve. This curve represents the demand for money at various rate of interest. The total supply of money is represented by a vertical line Ms. The equilibrium rate of interest is determined at that level. Where the demand for money is equal to supply of money. Given the demand for money when supply of money rises, rate of interest falls to OR. With a fall in money supply rate of interest rises. Similarly the liquidity preference may change given the supply of money. When liquidity preference shifts upward, given the supply money at the level on the rate of interest rises to the level OQ. Thus according to Keynes interact is purely a monetary phenomenon.

Source is here

Now watch a video....

Now read some more notes...

KEYNES’ LIQUIDITY PREFERENCE THEORY OF INTEREST

Keynes defines the rate of interest as the reward for parting with liquidity for a specified period of time. According to him, the rate of interest is determined by the demand for and supply of money.

Demand for money: Liquidity preference means the desire of the public to hold cash. According to Keynes, there are three motives behind the desire of the public to hold liquid cash: (1) the transaction motive, (2) the precautionary motive, and (3) the speculative motive. Transactions Motive: The transactions motive relates to the demand for money or the need of cash for the current transactions of individual and business exchanges. Individuals hold cash in order to bridge the gap between the receipt of income and its expenditure. This is called the income motive. The businessmen also need to hold ready cash in order to meet their current needs like payments for raw materials, transport, wages etc. This is called the business motive.

Precautionary motive: Precautionary motive for holding money refers to the desire to hold cash balances for unforeseen contingencies. Individuals hold some cash to provide for illness, accidents, unemployment and other unforeseen contingencies. Similarly, businessmen keep cash in reserve to tide over unfavourable conditions or to gain from unexpected deals. Keynes holds that the transaction and precautionary motives are relatively interest inelastic, but are highly income elastic.

The amount of money held under these two motives (M1) is a function (L1) of the level of income (Y) and is expressed as M1 = L1 (Y) Speculative Motive: The speculative motive relates to the desire to hold one’s resources in liquid form to take advantage of future changes in the rate of interest or bond prices. Bond prices and the rate of interest are inversely related to each other. If bond prices are expected to rise, i.e., the rate of interest is expected to fall, people will buy bonds to sell when the price later actually rises. If, however, bond prices are expected to fall, i.e., the rate of interest is expected to rise, people will sell bonds to avoid losses.

According to Keynes, the higher the rate of interest, the lower the speculative demand for money, and lower the rate of interest, the higher the speculative demand for money. Algebraically, Keynes expressed the speculative demand for money as M2 = L2 (r) Where, L2 is the speculative demand for money, and r is the rate of interest. Geometrically, it is a smooth curve which slopes downward from left to right. Now, if the total liquid money is denoted by M, the transactions plus precautionary motives by M1 and the speculative motive by M2, then M = M1 + M2. Since M1 = L1 (Y) and M2 = L2 (r), the total liquidity preference function is expressed as M = L (Y, r).

Supply of Money: The supply of money refers to the total quantity of money in the country. Though the supply of money is a function of the rate of interest to a certain degree, yet it is considered to be fixed by the monetary authorities. Hence the supply curve of money is taken as perfectly inelastic represented by a vertical straight line. Determination of the Rate of Interest: Like the price of any product, the rate of interest is determined at the level where the demand for money equals the supply of money. In the following figure, the vertical line QM represents the supply of money and L the total demand for money curve. Both the curve intersect at E2 where the equilibrium rate of interest OR is established.

Similarly at OR2 level of interest rate, the demand for money OM2 is greater than the supply of money OM. As a result, the rate of interest OR2 will start rising till it reaches the equilibrium rate OR. It may be noted that, if the supply of money is increased by the monetary authorities, but the liquidity preference curve L remains the same, the rate of interest will fall. If the demand for money increases and the liquidity preference curve sifts upward, given the supply of money, the rate of interest will rise.

Criticisms: Keynes theory of interest has been criticized on the following grounds:

1. It has been pointed out that the rate of interest is not purely a monetary phenomenon. Real forces like productivity of capital and thriftiness or saving by the people also play an important role in the determination of the rate of interest.

2. Liquidity preference is not the only factor governing the rate of interest. There are several other factors which influence the rate of interest by affecting the demand for and supply of investible funds.

3. The liquidity preference theory does not explain the existence of different rates of interest prevailing in the market at the same time.

4. Keynes ignores saving or waiting as a means or source of investible fund. To part with liquidity without there being any saving is meaningless.

5. The Keynesian theory only explains interest in the short-run. It gives no clue to the rates of interest in the long run.

6. Keynes theory of interest, like the classical and loanable funds theories, is indeterminate. We cannot know how much money will be available for the speculative demand for money unless we know how much the transaction demand for money is.

Read more...

Subscribe to:

Comments (Atom)